Back to all posts

June 17, 2026

TPRM for Fintech Startups: What Investors and Enterprise Clients Are Now Demanding

Why TPRM is a deal-stopper in 2026

Let's be direct: if you're a fintech founder pitching Series A or negotiating your first enterprise contract, your vendor stack is being scrutinized in ways it wasn't three years ago. Investors aren't just asking about ARR and runway. They're asking who has access to your systems, what your vendor review cycle looks like, and whether your compliance posture can survive a partner breach.

Third-party risk management has moved from back-office compliance work to a board-level and investor-level concern. The reasons are structural and they're accelerating. Nearly half of financial institutions experienced a third-party cyber event in the last year, with business continuity concerns among executives rising 64% between 2023 and 2025. A fintech startup without a defensible TPRM program is carrying unpriced risk on its balance sheet and sophisticated investors are starting to price it in.

Why US regulators made this personal for fintech

In June 2023, the Federal Reserve, FDIC, and OCC issued joint final guidance on third-party risk management the most significant regulatory update in this space in decades. The guidance explicitly names fintech companies as third-party relationships that banking organizations must assess under enhanced due diligence standards.

The guidance covers the full vendor lifecycle: planning, due diligence and selection, contract negotiation, ongoing monitoring, and termination. Critically, banking organizations using a third party do not transfer their regulatory responsibility they remain accountable for outcomes as if the activity were performed in-house.

What this means in practice

Enterprise and banking clients are now showing up to vendor reviews with structured questionnaires, asking for SOC 2 reports, requesting evidence of your own third-party risk processes, and building contract clauses that require ongoing compliance evidence. Fail any of those and the deal stalls or dies. For fintech startups operating across states and countries, each jurisdiction adds distinct regulatory requirements that demand a harmonized, auditable approach.

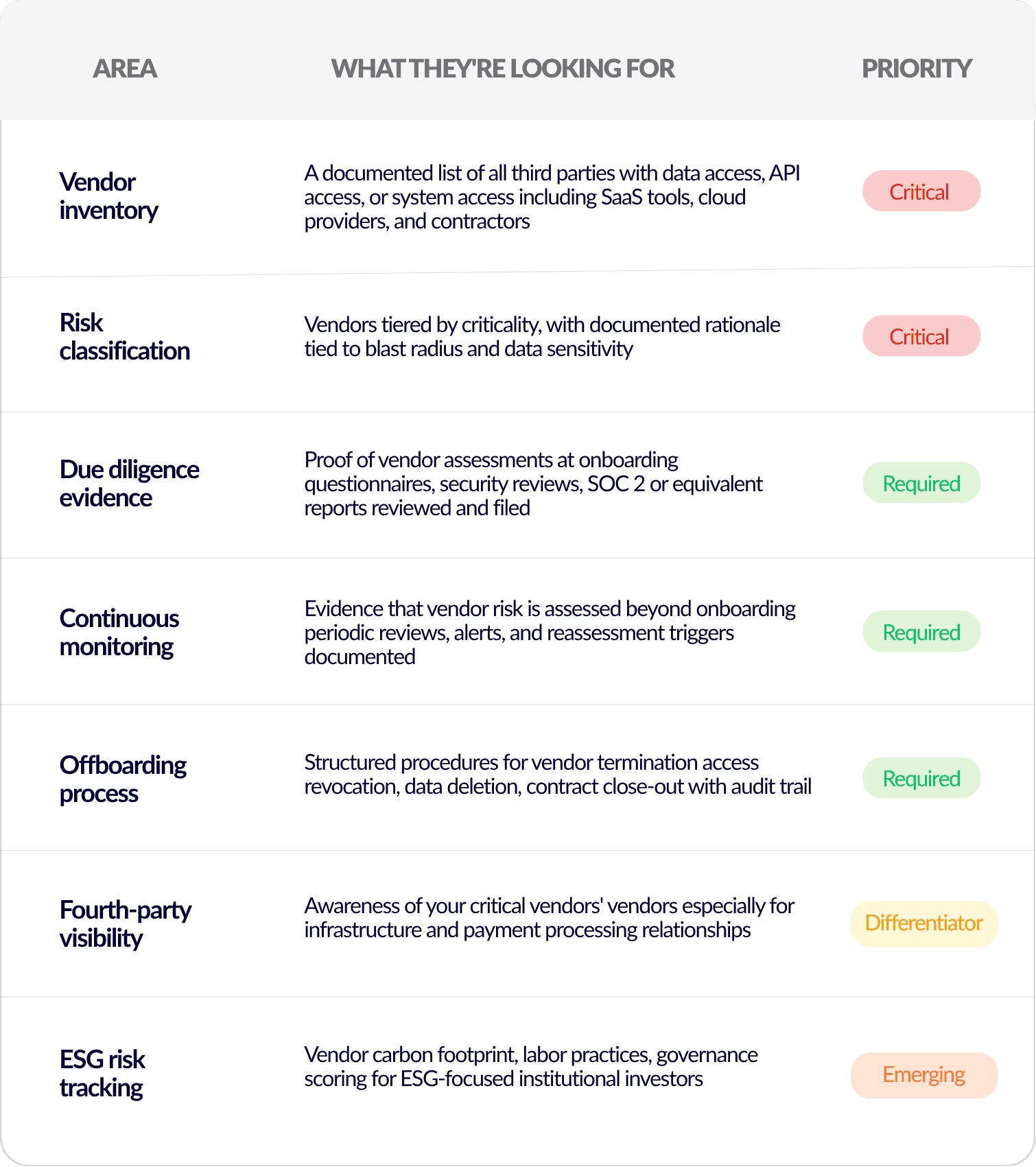

What investors are actually checking during due diligence

Multi-year assessment data published in 2026 shows that TPRM, alongside penetration testing gaps, ranks among the highest-risk domains flagged during investor due diligence consistently, across different portfolios. This reflects a broader governance challenge in how sponsors oversee risk across investments.

Here's what shows up on the investor checklist when they audit your vendor posture:

What enterprise clients require before they sign

Enterprise procurement teams have formalized their vendor security requirements. If your deal is above a certain size or if your buyer is in banking, healthcare, or insurance they are running TPRM due diligence on you as their vendor.

Clients and partners are increasingly requiring SOC 2 reports as part of vendor onboarding even smaller financial institutions and fintech firms are being pulled into this demand curve. Without external validation of trust, companies miss enterprise contracts, risk losing renewals, and face exposure during fundraising rounds.

The SOC 2 threshold shift

For early-stage companies, a SOC 2 Type I report used to be sufficient to pass a vendor questionnaire. That's changing fast. As you scale toward enterprise clients, Type II is increasingly the baseline expectation it shows that your controls operated effectively over 3–12 months, not just that they existed on paper at a single point in time.

Beyond SOC 2, enterprise clients in regulated sectors are asking fintech vendors to present evidence that the vendor itself manages its own third-party risks. The logic is simple: if your payment processor or cloud provider gets breached, can your enterprise client trace that risk back through your stack? If you can't answer that question, you're not enterprise-ready.

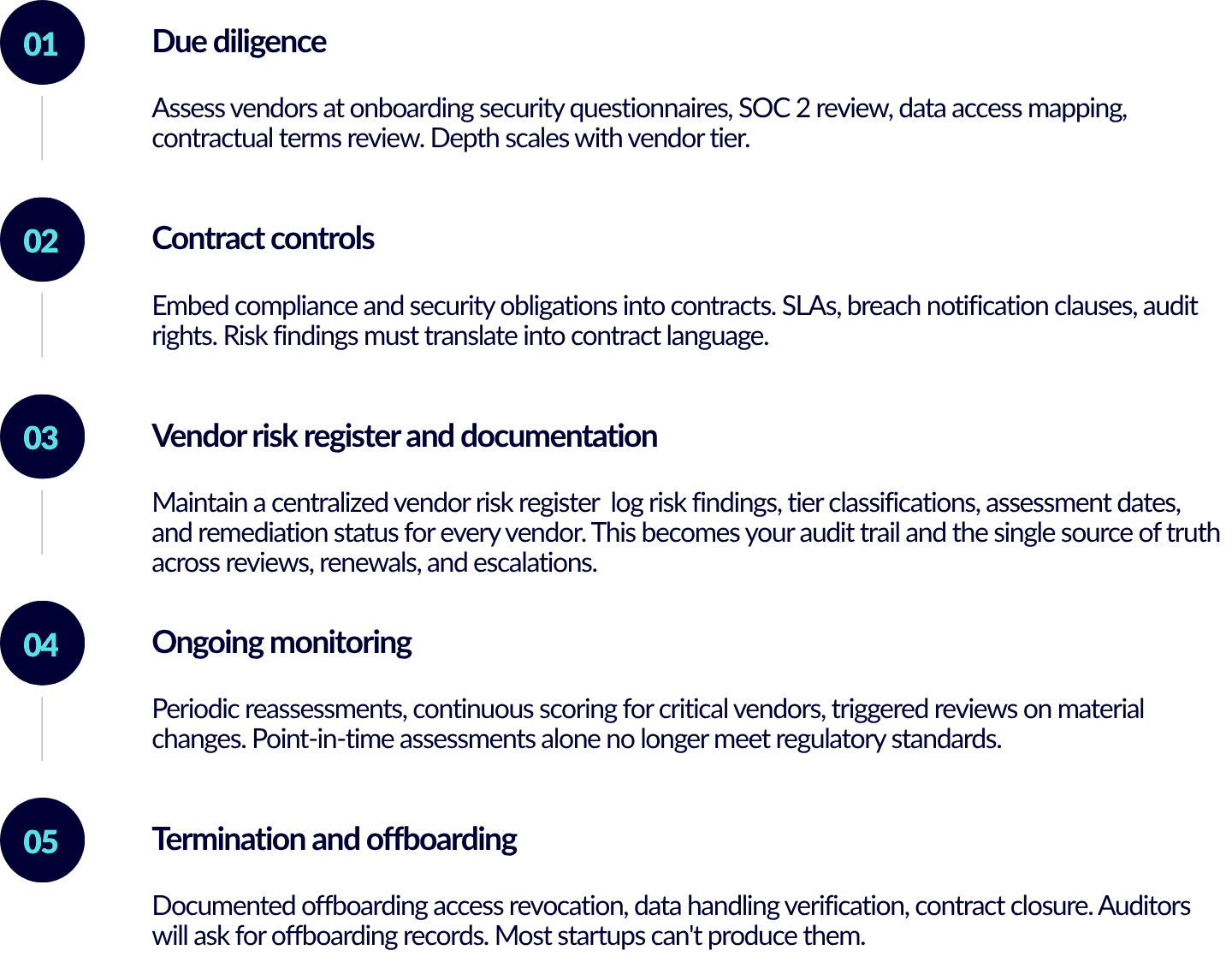

The five stages of a TPRM lifecycle

Building a TPRM program doesn't require a 50-person GRC team. What it requires is structure, documentation, and repeatability. Here's the standard lifecycle that maps to both regulatory expectations and investor scrutiny:

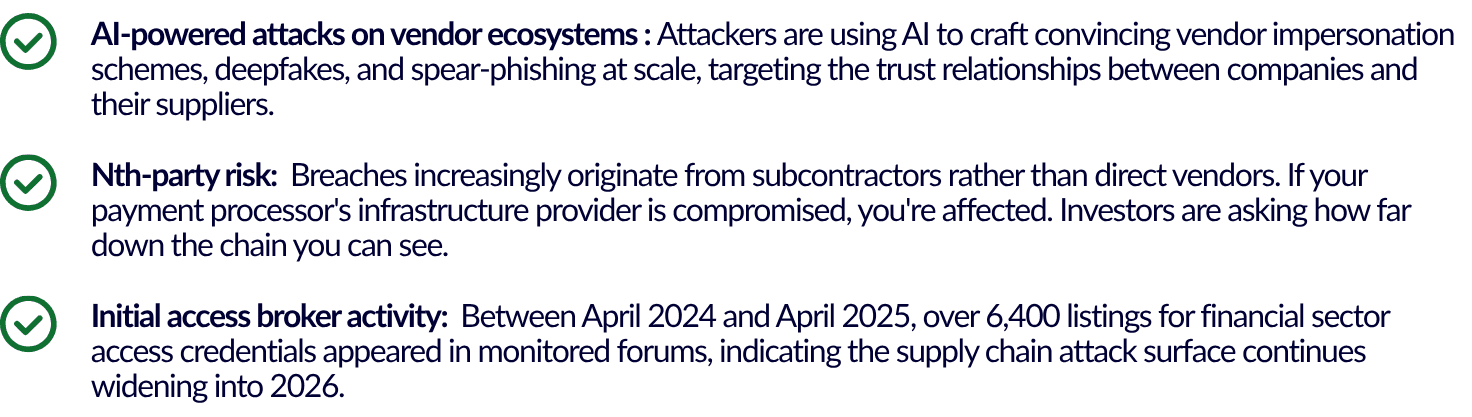

Emerging threats rewriting TPRM priorities in 2026

The threat landscape isn't static. Three new pressure points are showing up in investor conversations and enterprise security reviews this year:

AI as its own TPRM risk category

AI now ranks as the second-largest TPRM risk heading into 2025 across financial institution surveys. If your fintech platform uses AI vendors, AI APIs, or AI-assisted workflows and most modern fintechs do those relationships require their own risk tier. Expect enterprise clients and regulators to ask specifically about AI vendor governance in 2026 and beyond.

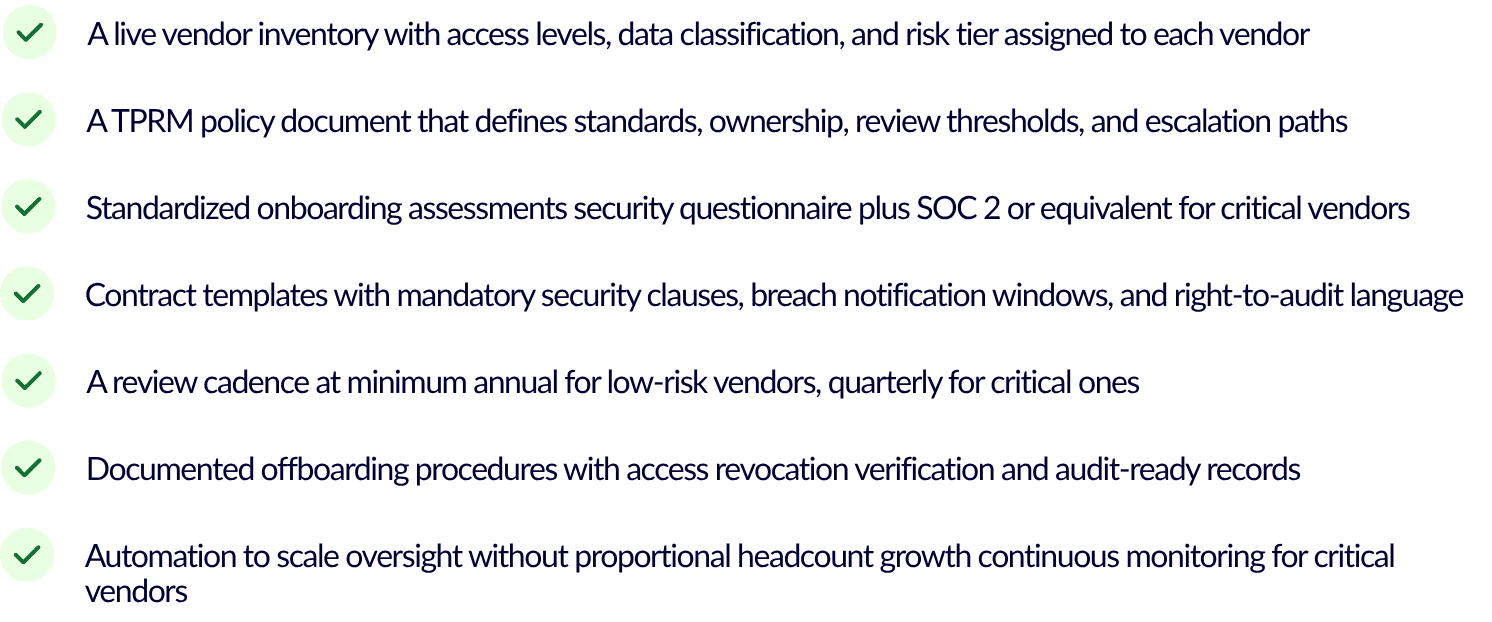

What a lean fintech TPRM program looks like

You don't need a dedicated GRC team to run a credible TPRM program. You need a defensible system one that produces evidence, stores it, and can be presented in an hour when a due diligence request lands.

TPRM as a revenue lever, not just a risk function

Here's the reframe that changes how founders think about this: TPRM isn't just a cost center. It's a sales enablement tool. A credible TPRM program means shorter enterprise sales cycles, fewer security questionnaire delays, faster procurement approvals, and a compliance posture that survives both investor scrutiny and customer audits.

Companies that can present their TPRM documentation in a structured, auditable format close enterprise deals faster. Procurement teams reward it. Investors price it. And in a landscape where a single third-party breach can derail investor confidence, trigger audits, and stunt growth the cost of not building it is significantly higher than the cost of building it early.

The fintechs that build TPRM infrastructure in their first 18 months don't have to rebuild it under pressure when a Series B term sheet arrives with a 30-day due diligence window.